Are Your Student Loans Up For IDR Recertification? Here Are Your Options While Applications Are Closed

Listen up, folks! If you're one of the millions of Americans drowning in student loan debt, you're probably already familiar with Income-Driven Repayment (IDR) plans. These plans are designed to make your monthly payments more manageable by capping them at a percentage of your discretionary income. But here's the deal—IDR recertification is coming up, and applications are temporarily closed. What does this mean for you? Let’s break it down.

Now, before we dive deep into the nitty-gritty, let’s get one thing straight. Student loans are no joke. They can feel like an anchor around your neck, especially if you're struggling to make ends meet. That’s why understanding your options during this recertification period is crucial. You don’t want to miss out on potential savings or end up in hot water with missed payments.

So, whether you’re a recent grad just starting out or someone who’s been paying off loans for years, this guide is here to help you navigate the IDR recertification process. We’ll cover everything from deadlines to alternative repayment strategies, so you can breathe a little easier. Let’s get started!

Here’s a quick overview of what we’ll be discussing:

- What is Income-Driven Repayment (IDR)?

- The IDR Recertification Process

- Why Are Applications Temporarily Closed?

- Your Options While Applications Are Closed

- How Does This Affect Your Monthly Payments?

- Can You Extend the Deadline?

- Tips for Successful Recertification

- Common Questions About IDR Recertification

- Exploring Alternative Repayment Plans

- Final Thoughts and Next Steps

What is Income-Driven Repayment (IDR)?

Let’s start with the basics. An Income-Driven Repayment (IDR) plan is like a lifeline for borrowers who are struggling to keep up with their student loan payments. Instead of paying a fixed amount every month, your payments are adjusted based on how much money you actually make. Cool, right?

There are several types of IDR plans, each with its own rules and benefits. Some of the most popular ones include:

- Income-Based Repayment (IBR)

- Pay As You Earn (PAYE)

- Revised Pay As You Earn (REPAYE)

- Income-Contingent Repayment (ICR)

These plans are designed to make repayment more manageable, especially for those with lower incomes or high loan balances. Plus, they often come with loan forgiveness after a certain number of years, which is a pretty sweet deal if you ask me.

Why Choose IDR Over Standard Repayment?

Well, it’s simple. Standard repayment plans usually require you to pay off your loans within 10 years, which can be tough if you’re not earning a ton of cash. With IDR, your payments are spread out over a longer period, sometimes up to 20 or 25 years, depending on the plan. This means lower monthly payments and less financial stress.

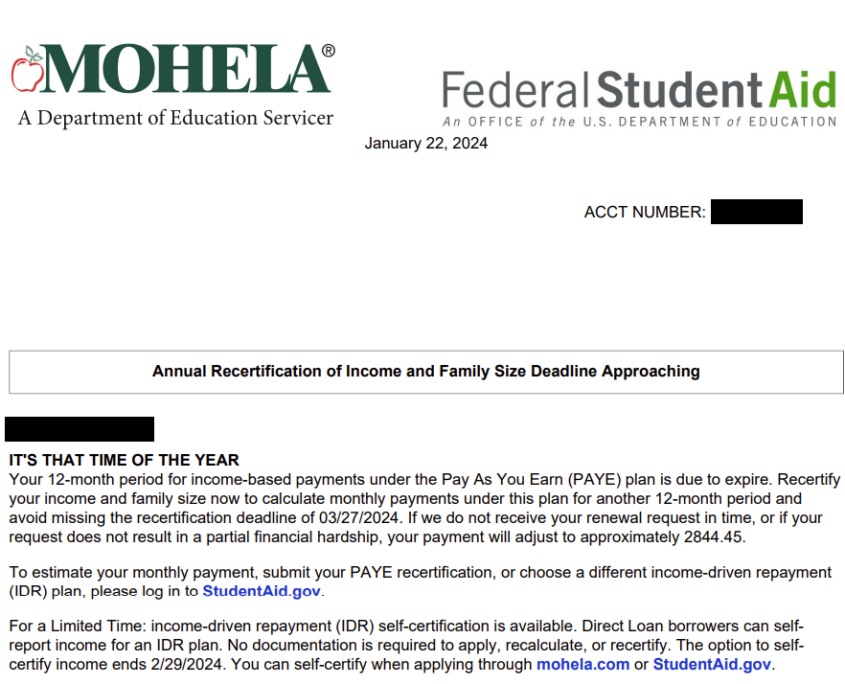

The IDR Recertification Process

Every year, borrowers on IDR plans need to recertify their income and family size. It’s kind of like a check-in to make sure your payments are still aligned with your current financial situation. But here’s the catch—this year, applications are closed for a bit. So what’s the deal?

How Does Recertification Work?

Normally, you’d log into your loan servicer’s website, update your income info, and submit any necessary documents. Your new payment amount would then be calculated based on your updated info. But since applications are temporarily closed, things are a bit different this time around.

Don’t panic though! There are still ways to ensure your payments stay on track while the system is down. We’ll get into those options in just a sec.

Why Are Applications Temporarily Closed?

Alright, let’s address the elephant in the room. Why are IDR applications closed right now? Turns out, the Department of Education is going through some updates to improve the system. Think of it like a software upgrade for your phone—it might be annoying in the short term, but it’s worth it in the long run.

These updates are aimed at streamlining the recertification process and making it easier for borrowers to manage their loans. So while it might feel like a hassle now, the goal is to make things smoother in the future.

What Does This Mean for You?

It means you’ll need to get creative with how you handle your recertification this year. Don’t worry—we’ve got you covered. Let’s talk about your options.

Your Options While Applications Are Closed

So, the big question—what can you do while IDR applications are closed? Here are a few strategies to keep your payments on track:

- Make Estimated Payments: If you’re not sure what your new payment amount will be, you can make estimated payments based on your previous year’s income. This will help you avoid late fees and keep your account in good standing.

- Reach Out to Your Loan Servicer: Sometimes, the best course of action is to pick up the phone and talk to someone. Your loan servicer can provide guidance on how to handle your specific situation and may even offer temporary relief options.

- Consider Temporary Forbearance: If you’re really struggling to make payments, you might qualify for a temporary forbearance. This allows you to pause your payments for a short period without penalty.

Remember, communication is key. The more proactive you are, the better off you’ll be when applications reopen.

How Does This Affect Your Monthly Payments?

Let’s talk numbers. If you don’t recertify on time, your payments could revert to the standard repayment plan. This means higher monthly payments and less flexibility. Not ideal, right?

That’s why it’s so important to stay on top of things, even if applications are closed. By making estimated payments or reaching out to your loan servicer, you can avoid any unpleasant surprises when the new payment amount is calculated.

What Happens If You Miss the Deadline?

If you miss the recertification deadline, your payments will automatically switch to the standard repayment plan. This could mean a significant increase in your monthly bill, so it’s definitely something you want to avoid.

Can You Extend the Deadline?

Here’s the thing—deadlines are deadlines. However, there are some situations where you might be able to get an extension. For example, if you’ve experienced a major life event like a job loss or medical emergency, you might qualify for additional time.

The best way to find out is to contact your loan servicer and explain your situation. They might be able to work with you to ensure your payments stay manageable.

Tips for Successful Recertification

Now that we’ve covered the basics, here are a few tips to help you ace the recertification process:

- Stay Organized: Keep all your income and family size info in one place so you’re ready to go when applications reopen.

- Set Reminders: Don’t rely on memory to keep track of deadlines. Set reminders on your phone or calendar to ensure you don’t miss anything important.

- Communicate Early and Often: If you’re unsure about anything, don’t hesitate to reach out to your loan servicer. They’re there to help!

By following these tips, you’ll be well-prepared to tackle recertification when the time comes.

Common Questions About IDR Recertification

Got questions? We’ve got answers. Here are some of the most common queries about IDR recertification:

- Q: Can I switch to a different IDR plan during recertification? A: Absolutely! If you think a different plan would work better for you, now’s the time to make the switch.

- Q: Do I need to recertify every year? A: Yep, annual recertification is a requirement for all IDR plans.

- Q: What happens if my income decreases? A: If your income goes down, your payments will likely decrease as well. That’s one of the perks of IDR plans!

Still have questions? Don’t hesitate to reach out to your loan servicer for clarification.

Exploring Alternative Repayment Plans

If IDR isn’t the right fit for you, there are other repayment options to consider. Here are a few:

- Graduated Repayment: Payments start low and increase every two years, making it a good option for those expecting a rise in income.

- Extended Repayment: Spreads payments over a longer period, usually 25 years, resulting in lower monthly payments.

- Consolidation: Combines multiple loans into one, simplifying the repayment process.

Each plan has its pros and cons, so it’s important to weigh your options carefully before making a decision.

Final Thoughts and Next Steps

Recertifying your IDR plan might seem like a headache, especially with applications closed, but it’s a crucial step in managing your student loan debt. By staying informed and proactive, you can ensure your payments stay manageable and avoid any unnecessary stress.

So, what’s next? Start gathering your income info, set those reminders, and don’t hesitate to reach out to your loan servicer if you have questions. Together, we can tackle this recertification process and get you one step closer to financial freedom.

And hey, don’t forget to share this article with anyone you know who might be in the same boat. The more we spread the word, the better off we’ll all be. Now go out there and crush those student loans!

3-Time NBA All-Star Ben Simmons Picks His NBA DPOY: Not Bam Adebayo Or Rudy Gobert

Damian Lillard's Injury Status For Warriors Vs Bucks: The Real Deal

Steph Curry Struggles In Warriors’ Ugly Loss To Nuggets: ‘He’s Exhausted’

IDR Recertification Postponed Until Fall 2024 Navigate Student

IDR Recertification How & When to Disclose Your

IDR Recertification in 2021 Save No Matter What Student Loan Planner