Cracking The Code On Student Loans Repayment: Your Ultimate Guide

Student loans repayment can feel like navigating a maze, but don’t panic, my friend. It’s not as scary as it sounds. Think of it as a puzzle waiting to be solved. With the right strategies, knowledge, and a little bit of patience, you can conquer this financial hurdle like a champ. So, buckle up and let’s dive into the nitty-gritty of paying off those pesky loans!

Let’s be real here—student loans are a reality for millions of people around the world. Whether you’re fresh out of college or have been juggling payments for years, understanding how to manage your student loans repayment is crucial. This isn’t just about numbers; it’s about taking control of your financial future.

In this article, we’ll break down everything you need to know about student loans repayment. From repayment plans to forgiveness programs, we’ve got you covered. So, grab a cup of coffee, get comfy, and let’s make sense of this whole situation together. Trust me, by the end of this, you’ll feel like a student loan repayment guru!

Understanding Student Loans Repayment Basics

Before we dive deep into the strategies, let’s first understand what exactly student loans repayment entails. Simply put, it’s the process of paying back the money you borrowed to fund your education. But here’s the kicker—it’s not just the principal amount you borrowed; it’s also the interest that accumulates over time.

Types of Student Loans

Not all student loans are created equal. There are two main types: federal loans and private loans. Federal loans are issued by the government and often come with more flexible repayment options. On the flip side, private loans are offered by banks or financial institutions and might not offer the same level of flexibility.

- Federal Loans: These include Direct Subsidized, Direct Unsubsidized, PLUS loans, and Perkins loans.

- Private Loans: These are typically offered by banks, credit unions, or online lenders.

Knowing the type of loan you have is crucial because it determines your repayment options and interest rates.

Repayment Plans: Choose Wisely

One of the most important decisions you’ll make is selecting the right repayment plan. The good news? There are plenty of options to choose from. Let’s explore some of the most popular ones.

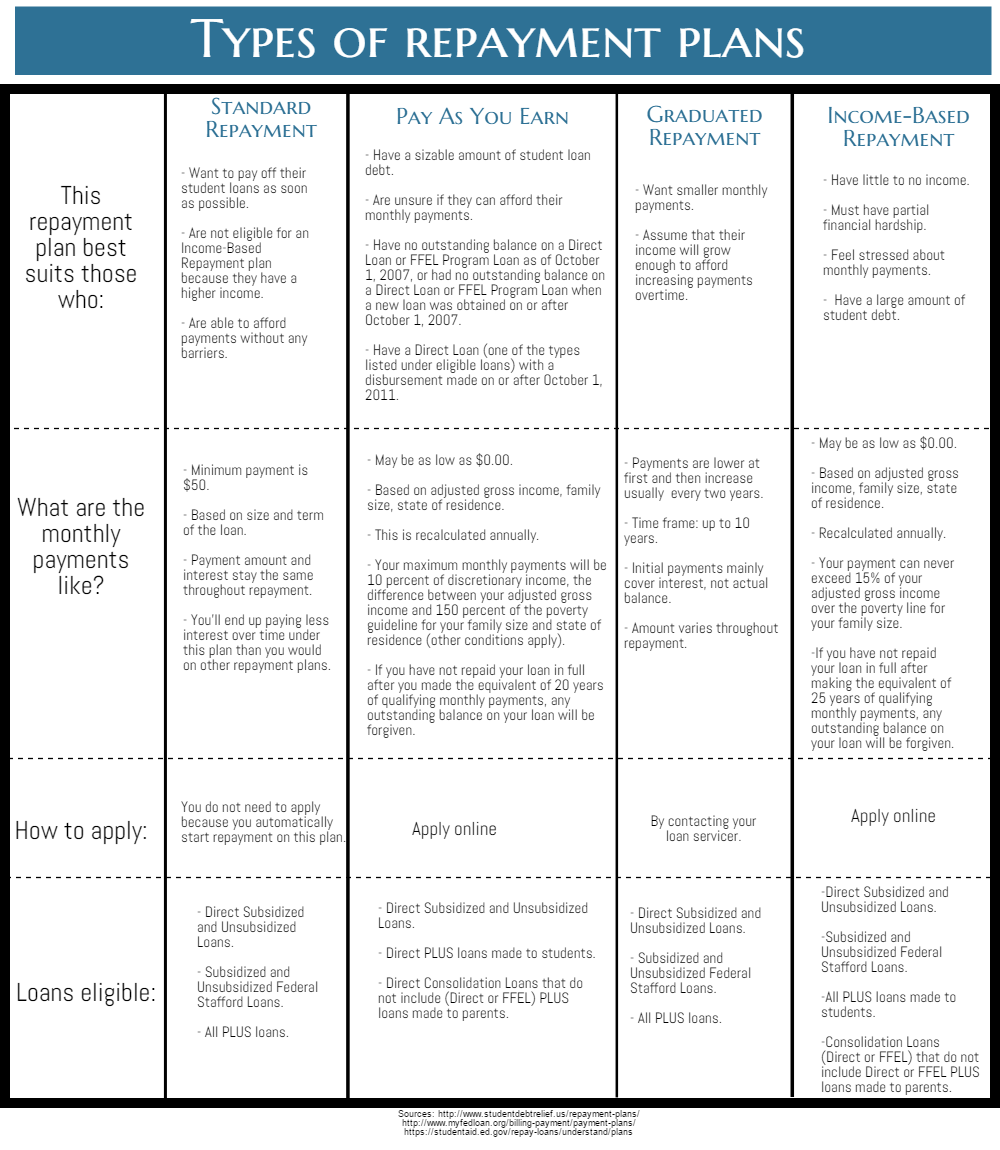

Standard Repayment Plan

This is the default plan for federal loans. You pay a fixed amount each month over a 10-year period. It’s straightforward and predictable, but it might not be the best option if you’re on a tight budget.

Income-Driven Repayment Plans

These plans adjust your monthly payments based on your income and family size. They’re a great option if you’re struggling to make ends meet. Some popular income-driven plans include:

- Income-Based Repayment (IBR)

- Pay As You Earn (PAYE)

- Revised Pay As You Earn (REPAYE)

- Income-Contingent Repayment (ICR)

Each plan has its own set of rules and benefits, so it’s important to do your research and choose the one that fits your financial situation.

Consolidation: Simplify Your Payments

If you’re juggling multiple loans, consolidation might be worth considering. Loan consolidation allows you to combine all your federal loans into a single loan with one monthly payment. It’s like turning chaos into order.

Here’s the deal: consolidation can simplify your life, but it might also extend the repayment period, which could result in paying more interest over time. So, weigh the pros and cons before making a decision.

When Should You Consolidate?

Consider consolidation if:

- You’re struggling to keep track of multiple loans.

- You want to switch to an income-driven repayment plan.

- You’re looking for a lower monthly payment.

But remember, consolidation isn’t a one-size-fits-all solution. It’s essential to evaluate your unique financial situation before taking this step.

Loan Forgiveness Programs: A Ray of Hope

Loan forgiveness programs are like the holy grail for borrowers. These programs offer relief by forgiving a portion or all of your student loan debt under certain conditions. Sounds too good to be true? Well, there are strings attached, but they’re definitely worth exploring.

Public Service Loan Forgiveness (PSLF)

PSLF is designed for borrowers who work in public service jobs, such as teachers, nurses, or government employees. If you make 120 qualifying payments while working full-time in a public service job, the remaining balance of your loans can be forgiven. It’s a win-win situation if you qualify.

Teacher Loan Forgiveness

This program forgives up to $17,500 of your Direct or FFEL Program loans if you teach full-time for five consecutive years in a low-income school or educational service agency. It’s a great incentive for educators who dedicate their lives to shaping young minds.

Strategies to Accelerate Repayment

While repayment plans and forgiveness programs are great options, sometimes you just want to get rid of those loans faster. Here are some strategies to help you accelerate your student loans repayment:

- Make Extra Payments: Even small additional payments can make a big difference over time.

- Refinance Your Loans: If you have a good credit score, refinancing could lower your interest rate and reduce your monthly payments.

- Use Windfalls Wisely: Got a tax refund or bonus? Put it towards your loans instead of splurging on unnecessary expenses.

- Side Hustle: Take up a part-time job or freelance work to generate extra income specifically for loan repayment.

Remember, every little bit helps. The sooner you pay off your loans, the less interest you’ll pay in the long run.

Dealing with Financial Hardship

Life happens, and sometimes you might find yourself in a tough spot financially. If you’re struggling to make your student loan payments, don’t panic. There are options available to help you get back on track.

Deferment and Forbearance

Deferment and forbearance allow you to temporarily pause or reduce your loan payments. Deferment is typically available if you’re unemployed, returning to school, or serving in the military. Forbearance, on the other hand, is an option if you’re facing financial hardship but don’t qualify for deferment.

While these options can provide short-term relief, keep in mind that interest may continue to accrue during the deferment or forbearance period.

Common Mistakes to Avoid

When it comes to student loans repayment, there are a few common mistakes that can cost you big time. Let’s take a look at some of them:

- Ignoring Your Loans: Avoiding the problem won’t make it go away. Ignoring your loans can lead to default, which has serious consequences.

- Not Exploring All Options: Don’t settle for the default repayment plan without exploring other options that might better suit your needs.

- Refinancing Without Careful Consideration: Refinancing can be a great option, but it’s important to weigh the pros and cons before making a decision.

By avoiding these common pitfalls, you can set yourself up for success in your student loans repayment journey.

Building a Budget: The Foundation of Repayment Success

A solid budget is the foundation of any successful repayment plan. It helps you prioritize your expenses and allocate funds towards paying off your loans. Here’s how to create a budget that works for you:

- Track Your Expenses: Know where your money is going and identify areas where you can cut back.

- Set Realistic Goals: Be honest about what you can afford to pay each month.

- Automate Payments: Set up automatic payments to ensure you never miss a deadline.

A well-planned budget can make the repayment process less stressful and more manageable.

Staying Motivated: Keep Your Eyes on the Prize

Paying off student loans can be a long and sometimes frustrating journey. But staying motivated is key to achieving your goals. Here are a few tips to keep you inspired:

- Celebrate Small Wins: Acknowledge every milestone, no matter how small.

- Visualize the End Goal: Imagine the freedom and peace of mind that come with being debt-free.

- Join a Community: Connect with others who are on the same journey for support and encouragement.

Remember, every step you take brings you closer to financial freedom.

Conclusion: Taking Control of Your Financial Future

Student loans repayment doesn’t have to be a daunting task. With the right strategies, tools, and mindset, you can conquer this challenge and take control of your financial future. From choosing the right repayment plan to exploring forgiveness programs, there are plenty of options available to help you succeed.

So, what are you waiting for? Take action today and start your journey towards becoming debt-free. Leave a comment below and let me know which strategy resonates with you the most. And don’t forget to share this article with your friends who might be struggling with student loans repayment. Together, we can make a difference!

Table of Contents

- Understanding Student Loans Repayment Basics

- Types of Student Loans

- Repayment Plans: Choose Wisely

- Standard Repayment Plan

- Income-Driven Repayment Plans

- Consolidation: Simplify Your Payments

- When Should You Consolidate?

- Loan Forgiveness Programs: A Ray of Hope

- Public Service Loan Forgiveness (PSLF)

- Teacher Loan Forgiveness

- Strategies to Accelerate Repayment

- Dealing with Financial Hardship

- Deferment and Forbearance

- Common Mistakes to Avoid

- Building a Budget: The Foundation of Repayment Success

- Staying Motivated: Keep Your Eyes on the Prize

Justin Eichorn: The Man Revolutionizing Digital Marketing

Duplicity Tyler Perry: The Untold Stories And Fascinating Facts

Pascal Siakam: The Rise Of A Modern-Day Basketball Star

Loan Repayment Schedule, Student Loan Repayment Template, Loan

Student loan repayment options

🆕 The new annual... Student Loans Company Repayment